SMA algorithm that accepts ‘series’ length

Indie’s standardindie.algorithms.Sma algorithm has a length parameter which cannot be dynamically changed. Its common usage looks like this: Sma.new(self.close, length=12), where the length parameter is typically a literal constant. While it is possible for the length to be a variable calculated at the time of indicator initialization or even during calculation over bars/candles, the general rule that should not be broken is as follows: once set, the value of the length parameter should not change. Otherwise, the algorithm breaks internally and starts giving inaccurate results*.

Sometimes, greater flexibility is needed. Fortunately, there is a way to achieve this, and this indicator with MySma algorithm demonstrates it. The algorithm is based on properties derived from prefix sums. Let’s look at an example to see how it works. Suppose we have a source series of values, src, like this:

src = …, 2, 7, 5, 4, 3, 9, 6

Think of this series as a series of close prices of some instrument on a chart. The last (i.e., current) value of this series is 6, which is accessed in Indie with the expression src[0].

To calculate the SMA with a length period, we simply divide the sum of length elements by the length value. The sum calculation seems straightforward, but it can be inefficient. For example, sum(src, length=3) is calculated as 3 + 9 + 6 = 18. This calculation is CPU-intensive, and the larger the length value, the more computationally expensive it becomes (the time complexity of this calculation is linear). This isn’t a big issue if the length is constant. However, consider a use case where length may vary from 2 to 300, and the size of the src series is around 20,000 bars, requiring SMA (and thus sum) calculations at every bar of this dataset. That would involve a lot of sum operations.

If we use prefix sums, which in Indie can be calculated with a cs = CumSum.new(src, length) statement, we can calculate sums in constant time (which is faster):

cs = …, 2, 9, 14, 18, 21, 30, 36

Calculation of any sum with any length using the cs series is as simple as subtracting two numbers. For example, sum(src, length=3) = cs[0] - cs[3] = 36 - 18 = 18. Let’s calculate sums with a few different lengths:

sum(src, length=4) = cs[0] - cs[4] = 36 - 14 = 22, which is the same as4 + 3 + 9 + 6 = 22sum(src, length=5) = cs[0] - cs[5] = 36 - 9 = 27, which is the same as5 + 4 + 3 + 9 + 6 = 27

sum(src, length) = cs[0] - cs[length]

In this indicator, there are three SMA plot lines:

- The thin green and thin red lines both use the

indie.algorithm.Smafrom the standard library. They use different but constantlengthparameters:short_lenandlong_len. These two plots serve as references with which we compare the third plot. - The thick light blue line uses the

MySmaalgorithm described above, which is based on the prefix sums approach. MySma can accept a ‘series’ length, and depending on runtime conditions, eithershort_lenorlong_lenis passed to it.

SMA algorithm that accepts length

Green/Red Bar Counts - usage example of indie.MutSeries[T] generic class

Indie includes generic series types:indie.Series[T] and indie.MutSeries[T]. The float-types indie.SeriesF and indie.MutSeriesF are still available as aliases for indie.Series[float] and indie.MutSeries[float], respectively.

The “Green/Red Bar Counts” indicator demonstrates the usage of the new generic class indie.MutSeries[T], which is instantiated with T as the int type. The generic type parameter T can be any (well, almost any) Indie type, such as bool, str, etc.

Green/Red Bar Counts - usage example of indie.MutSeries[T] generic class

Sma-Ema Crossover - usage example of indie.Var[T]

Theindie.Var[T] container functions similarly to indie.MutSeries[T], but it has a single-value history depth, making it ideal for storing and updating the current state without accumulating historical values. Although indie.Var[T] does not store historical values, it differs significantly from a primitive field of type T of an Algorithm/Context or a global variable. The key difference lies in its behavior during real-time calculations. indie.Var[T] retains only the values set on closing bar updates, reverting to the previous value before each intrabar update.

The “SMA-EMA Crossover” indicator demonstrates the use of indie.Var[T] through the algorithm CrossoverWithVar, which detects and retains values on specific crossover events. It also includes the algorithm CrossoverWithSeries to illustrate how to achieve the same result without using indie.Var[T].

Sma-Ema Crossover - usage example of indie.Var[T]

Green/Red Bar Count - usage example of indie.Var[T]

This update of “Green/Red Bar Counts” indicator showcases theindie.Var[T] container usage.

In this implementation:

- State Tracking: The

indie.Var[T]container counts consecutive green (up) or red (down) bars without retaining any history.indie.Var[T]is ideal here since it efficiently holds only the most recent value, unlike indie.MutSeries[T], which maintains a historical sequence of values.

Why Use indie.Var Instead of a Simple Float or Integer?

Unlike using a singlefloat or int, indie.Var is fully compatible with Indie’s series-based environment, where values update bar by bar. Plain variables would reset on each new bar calculation, causing them to lose their previous state. Moreover, indie.Var ensures that values persist correctly in both historical and real-time data. A simple local number variable would reset or lack the ability to update accurately in real-time, making it unsuitable for cumulative calculations. In contrast, indie.Var provides stable, consistent updates across all bars.

Key Differences with the Previous Version: General Transformation from MutSeries to Var

In cases where only the latest value is required without retaining historical data, you can convert code from indie.MutSeries to indie.Var by following these general rules:

- Replace

MutSeries.new()withVar.new():

my_var = Var[float].new(0) # instead of my_series = MutSeries[float].new(0)

- Use

.get()and.set()instead of indexing:

var_value = my_var.get() # instead of series_value = my_series[0]

my_var.set(new_value) # instead of my_series[0] = new_value

Green/Red Bar Count - usage example of indie.Var[T]

Median Algorithm (written with Indie v4 classes)

This is an example of an Indie algorithm that uses class syntax, introduced in the language since version 4. The Median class of this indicator inherits from theindie.Algorithm base class. It has two methods: the __init__ constructor and calc. It is essential that the __init__ constructor is executed only once during the creation of the indicator. This makes it a good location to create all objects that hold the algorithm’s state, ensuring these objects do not lose their data when a candle update arrives (triggering the calc method). The stateful objects (fields) are:

self._sorted_vals: list[float]- A list of the last length values of the input series src. The algorithm keeps those values ordered.self._prev_src_val: float- The previous value of the last element in the src series.self._bar_count: int- A counter for bars that we use to detect when a new bar arrives.

length values of the src series and keep these values in sorted order. With such an array, the median is easily calculated as the value in the middle of it.

Median Algorithm (written with Indie v4 classes)

Custom VWAP - usage example of indie.Schedule class

The “Custom VWAP” indicator demonstrates the usage of theSchedule class. If we don’t want to reset VWAP at the start of each new default trading day (using the ‘Session’ option of the anchor parameter), we can create a custom schedule to define the reset time.

For example, by default, the VWAP reset time for ‘BTC/USDT’ is at 00:00 UTC. However, we may want to change this reset time to 00:00 in our chosen timezone (e.g., ‘America/New_York’ for this indicator).

Key Points:

- The custom schedule is defined in the

__init__function because creating it on each bar in theContext.calcfunction is resource-inefficient. Alternatively, theContext.pre_calcfunction can be used for schedule definition if we need to access data fromself.infoorself.trading_session. - The is_same_period method (for both

ScheduleandSessionoptions) is used to detect whether two timestamps belong to the same schedule period or fall on different days.

Custom VWAP - usage example of indie.Schedule class

Volume spike marker - usage example of Markers

This indicator highlights bars where the trading volume significantly exceeds the recent average. A text marker is plotted above the bar if the current volume is more than twice the 20-bar moving average. It’s a simple tool to help spot unusual activity and potential breakout points. Markers are visual elements that allow you to highlight important moments on the chart by displaying icons, shapes, or text as part of your indicator. Using markers is just as easy as other plots, you need to declare them in decorators@plot.marker(...) and return the corresponding value plot.Marker(...) from the Main function. You can use different styles, colors, and sizes of markers, and you can display different text.

Let’s take a closer look at the available options in decalaration decorator:

Volume spike marker - usage example of Markers

Different types of markers - yet another example of Markers usage

Let’s look at another indicator that draws several series of markers of different shapes and colors. Full code:Different types of markers - yet another example of Markers usage

float, the type will be implicitly converted to plot.Marker:

plot.Maker object:

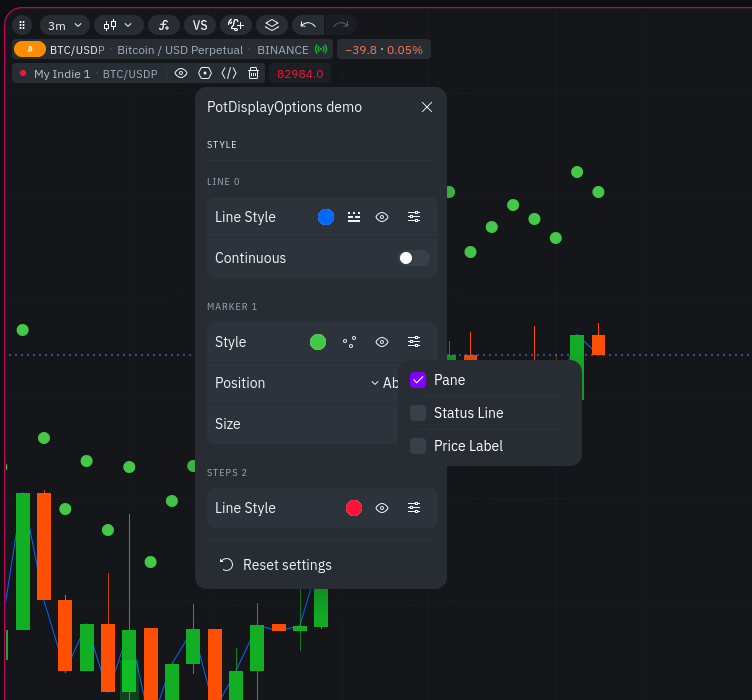

Plot display options - hide the unnecessary parts from the chart

When the indicator draws many different lines, the chart may become “too noisy”. It often happens that you don’t need to display all the chart elements on the chart, for example, you need to leave only the line without its numeric value, or vice versa, leave only the number but hide the line. And then the plot display options come to the rescue. You can configure this via the UI in the indicator settings:

Plot display options - hide the unnecessary parts from the chart

- pane - to display an element (line, markers, etc.) on a chart pane;

- status_line - to display a numeric value next to the name and settings of the indicator;

- price_label - to display a numeric value on the ordinate axis of the graph.

Background and bar colors - colorize your chart

This indicator demonstrates how to usebackground and bar_color plots to colorize the chart background and candlesticks based on custom conditions. It also shows that these plot types can be seamlessly combined with other plot types like lines and drawings.

This approach is useful for creating visual indicators that highlight specific market conditions, patterns, or zones directly on the chart.